If you’re a business owner, contractor, or self-employed professional, understanding workers’ compensation exemptions can save you from costly mistakes and compliance issues. While most employers are legally required to carry workers’ compensation insurance, not everyone falls under these requirements. Certain individuals and businesses may qualify for exemptions based on their employment status, industry, ownership structure, or state regulations.

The challenge is that exemption rules vary significantly across states, and assuming you’re exempt without verification can lead to fines, lawsuits, and unexpected financial liability. Whether you’re trying to determine if you need coverage, exploring exemption options, or ensuring your business remains compliant, knowing who qualifies for a workers’ compensation exemption is essential.

In this article, we’ll break down the most common exemptions, explain how they work, and help you understand when opting out may or may not be the right decision.

What Is Workers’ Compensation Insurance?

Workers’ compensation insurance is a type of coverage that helps protect employees and employers when a work-related injury or illness occurs. It provides financial support for medical expenses, lost wages, rehabilitation costs, and, in some cases, death benefits for an employee’s family.

In exchange for these benefits, employees generally give up the right to sue their employer for workplace injuries. This system creates a safety net for workers while helping businesses avoid costly legal disputes.

How Workers’ Compensation Insurance Works?

When an employee suffers an injury or illness arising from their job, workers’ compensation insurance may cover:

- Medical treatment and hospital expenses

- Partial wage replacement during recovery

- Disability benefits

- Rehabilitation services

- Death benefits for dependents

The specific benefits available depend on state laws and the circumstances of the claim.

Why Most Employers Are Required to Carry Workers’ Compensation Insurance?

Most states require employers to maintain workers’ compensation coverage once they hire employees. These laws are designed to ensure injured workers receive prompt financial assistance without needing to prove fault.

Failure to carry required coverage can result in significant penalties, fines, lawsuits, and even business shutdowns in some states.

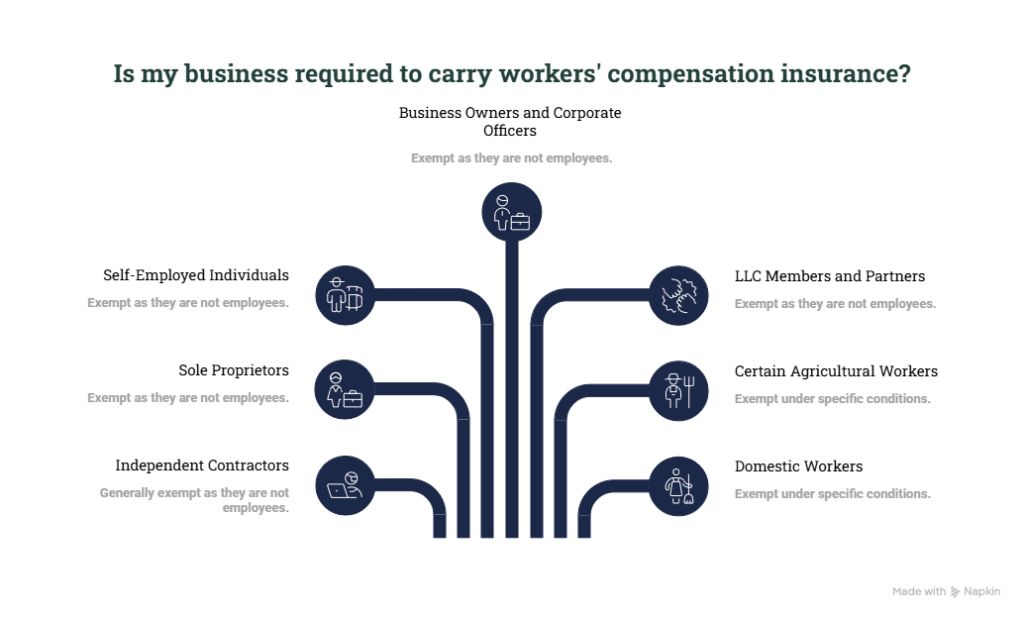

Who Is Exempt from Workers’ Compensation Insurance?

Certain individuals and businesses may be exempt from workers’ compensation insurance requirements depending on state regulations, industry classifications, and employment status.

Generally, workers’ compensation exemptions often apply to:

- Independent contractors

- Sole proprietors

- Self-employed individuals

- Business owners and corporate officers

- LLC members and partners

- Certain agricultural workers

- Domestic workers

- Volunteers

- Real estate agents

- Casual laborers

However, exemption rules vary widely by state. An individual who qualifies for an exemption in one state may be required to carry coverage in another. For this reason, employers should always verify state-specific requirements before assuming an exemption applies.

Categories of Individuals Commonly Exempt from Workers’ Compensation Coverage

While workers’ compensation laws are designed to protect employees, several groups are frequently excluded from mandatory coverage requirements.

1. Independent Contractors

Independent contractors are among the most commonly exempt workers because they operate as separate businesses rather than employees.

Businesses generally do not provide workers’ compensation coverage for independent contractors, provided the worker meets the legal criteria for contractor status.

However, worker classification is closely monitored by state agencies. If a contractor is found to function as an employee, the employer may face penalties, back premiums, and legal liability.

2. When Contractors May Still Need Coverage

Some industries, particularly construction, require independent contractors to carry their own workers’ compensation insurance. Additionally, clients may require proof of coverage before awarding contracts.

3. Sole Proprietors

Sole proprietors are often exempt because they own and operate their businesses without employees.

Although coverage may not be legally required, many sole proprietors choose to purchase workers’ compensation insurance voluntarily. A workplace injury could otherwise leave them responsible for medical bills and lost income.

4. Business Owners, Partners, and LLC Members

Many states allow business owners to exempt themselves from workers’ compensation requirements.

Common exemptions may include:

- Corporate officers

- LLC members

- Business partners

- Company shareholders

In many cases, owners must file an exemption certificate or election form with the appropriate state agency to opt out legally.

Are Small Businesses Exempt from Workers’ Compensation Insurance?

One of the most common misconceptions is that all small businesses are exempt from workers’ compensation requirements. In reality, the answer depends on state law and the number of employees a business has.

Some states require coverage as soon as a business hires its first employee, while others establish minimum employee thresholds before coverage becomes mandatory.

For example, certain states require workers’ compensation insurance for:

- One employee

- Three employees

- Five employees

- Industry-specific workforce thresholds

Additionally, construction companies often face stricter requirements regardless of company size.

Even if a small business qualifies for an exemption, obtaining coverage may still provide valuable protection against workplace injury costs and potential liability claims.

Before relying on an exemption, business owners should review their state’s workers’ compensation regulations and confirm whether employee count, payroll size, or industry classification affects their obligations.

Workers’ Compensation Exemptions by State

Workers’ compensation laws are regulated at the state level, which means exemption rules can vary significantly across the country. An exemption that applies in one state may not apply in another, making it essential for employers and workers to understand their local requirements.

For example, some states allow business owners and corporate officers to opt out of coverage, while others impose stricter participation requirements. Likewise, employee thresholds, agricultural exemptions, and contractor classifications often differ from state to state.

Why State Laws Matter?

State laws determine:

- Who qualifies as an employee

- Which businesses must carry coverage

- Available owner exemptions

- Industry-specific requirements

- Penalties for non-compliance

Because these rules frequently change, businesses should regularly review their state’s workers’ compensation regulations.

Examples of Common State-Specific Exemptions

While requirements vary, many states offer exemptions for:

- Sole proprietors

- Corporate officers

- LLC members

- Partners in a partnership

- Agricultural workers

- Domestic workers

- Real estate agents

- Independent contractors

Texas is often highlighted because most private employers are not legally required to carry workers’ compensation insurance. However, employers who opt out may face increased liability exposure if workplace injuries occur.

How to Verify Your State’s Requirements?

To determine whether you qualify for an exemption:

- Review your state’s workers’ compensation laws.

- Verify worker classifications.

- Check employee threshold requirements.

- Determine whether exemption forms must be filed.

- Consult an insurance professional or legal advisor when necessary.

Can Employers Legally Exempt Employees From Workers’ Compensation?

In most situations, employers cannot simply choose to exempt employees from workers’ compensation coverage when state law requires protection.

Workers’ compensation laws are designed to safeguard employees, and employers generally cannot avoid coverage obligations through private agreements or verbal arrangements.

Employee Waivers and Opt-Out Agreements

Many business owners mistakenly believe employees can sign a waiver declining workers’ compensation benefits. In most states, such agreements are not legally enforceable.

Even if an employee agrees to waive coverage, the employer may still be responsible for providing benefits and complying with state regulations.

Limited Exceptions

Certain exemptions may apply when workers are legally classified as:

- Independent contractors

- Business owners

- Corporate officers

- Partners

- LLC members

However, these exemptions typically require compliance with state-specific filing and eligibility requirements.

Risks of Improper Exemptions

Incorrectly exempting employees can lead to:

- Regulatory penalties

- Backdated insurance premiums

- Employee injury claims

- Civil lawsuits

- Increased insurance audits

For most businesses, proper worker classification is the key factor in determining coverage obligations.

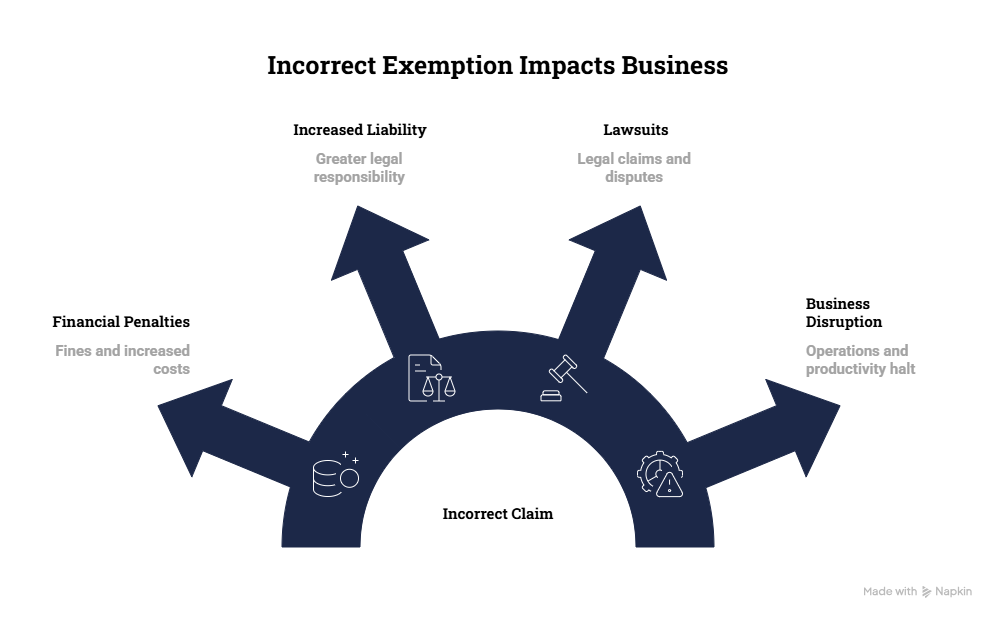

What Happens If You Incorrectly Claim a Workers’ Compensation Exemption?

Claiming an exemption without meeting legal requirements can create serious financial and legal consequences for a business.

Insurance carriers and state agencies routinely investigate worker classifications and exemption claims, especially after workplace injuries occur.

Financial Penalties

Businesses may be required to pay:

- State fines

- Backdated insurance premiums

- Interest charges

- Administrative penalties

In some states, penalties can reach thousands of dollars per violation.

Increased Liability Exposure

Without valid workers’ compensation coverage, employers may become directly responsible for:

- Medical expenses

- Lost wages

- Rehabilitation costs

- Legal settlements

This can create significant financial strain, particularly for small businesses.

Lawsuits and Legal Claims

One of the primary advantages of workers’ compensation insurance is protection from most employee injury lawsuits.

When a business improperly claims an exemption, injured workers may pursue legal action seeking compensation beyond standard workers’ compensation benefits.

Business Disruption

Serious compliance violations can result in:

- Stop-work orders

- License issues

- State investigations

- Reputational damage

These consequences often cost far more than maintaining proper coverage.

Why Some Exempt Individuals Still Choose Workers’ Compensation Coverage

Being exempt does not necessarily mean that going without protection is the best option. Many business owners, contractors, and self-employed professionals voluntarily purchase workers’ compensation insurance to protect themselves financially.

Protection Against Unexpected Medical Costs

A workplace injury can result in substantial medical expenses, surgeries, therapy, and ongoing treatment.

Without coverage, exempt individuals are typically responsible for these costs themselves.

Income Replacement During Recovery

For self-employed individuals, an injury often means lost income. Workers’ compensation coverage may help replace a portion of earnings while recovery takes place.

Meeting Client and Contract Requirements

Many companies require contractors and subcontractors to provide proof of workers’ compensation insurance before beginning work.

Voluntary coverage can help:

- Win larger contracts

- Meet vendor requirements

- Improve business credibility

Additional Protection for High-Risk Industries

Workers in industries such as:

- Construction

- Roofing

- Landscaping

- Manufacturing

- Agriculture

often face greater injury risks. Even when exempt, coverage can provide valuable financial protection and peace of mind.

Competitive Advantage

Businesses that maintain proper insurance coverage often appear more professional and trustworthy to clients, partners, and project owners.

For many exempt individuals, workers’ compensation insurance is less about compliance and more about protecting their livelihood, reputation, and long-term business success.

How to Apply for a Workers’ Compensation Exemption?

If you qualify for a workers’ compensation exemption, you may need to complete specific paperwork before you can legally opt out of coverage. The process varies by state, but most jurisdictions follow a similar procedure.

Failing to file the proper documentation can result in compliance issues, even if you otherwise meet exemption requirements.

Step 1: Determine Your Eligibility

Before applying, verify whether your state allows exemptions for your business structure or occupation.

Commonly eligible individuals include:

- Sole proprietors

- Corporate officers

- LLC members

- Business partners

- Certain independent contractors

Eligibility requirements often depend on ownership percentage, job duties, and business type.

Step 2: Complete the Required Forms

Many states require applicants to submit exemption forms through a workers’ compensation board, labor department, or insurance agency.

The application may require:

- Business information

- Ownership documentation

- Tax identification details

- Proof of business status

Step 3: Obtain an Exemption Certificate

Once approved, you may receive an exemption certificate confirming your status.

Businesses often use this document to:

- Demonstrate compliance

- Satisfy client requirements

- Avoid unnecessary premium charges

- Verify exemption during insurance audits

Step 4: Renew the Exemption When Required

Some states require exemption certificates to be renewed periodically.

Business owners should monitor expiration dates and ensure all records remain up to date to avoid accidental non-compliance.

Common Mistakes Businesses Make Regarding Workers’ Compensation Exemptions

Many employers assume they qualify for an exemption without fully understanding the legal requirements. Unfortunately, even small mistakes can result in audits, penalties, and costly claims.

Misclassifying Employees as Independent Contractors

This is one of the most common compliance issues.

Simply labeling a worker as an independent contractor does not automatically make them exempt. State agencies evaluate factors such as:

- Degree of control

- Work schedules

- Payment methods

- Job responsibilities

If a worker is determined to be an employee, the business may be responsible for unpaid premiums and penalties.

Assuming Small Businesses Are Automatically Exempt

Many business owners believe workers’ compensation laws only apply to large companies.

In reality, numerous states require coverage as soon as the first employee is hired.

Failing to File Exemption Paperwork

Qualifying for an exemption and officially obtaining one are often two different things.

Some states require formal exemption filings before the exemption becomes valid.

Ignoring State Law Changes

Workers’ compensation regulations evolve regularly. Employee thresholds, exemption criteria, and reporting requirements may change over time.

Businesses should review applicable laws annually to remain compliant.

Neglecting Documentation

Employers should maintain records such as:

- Contractor agreements

- Exemption certificates

- Payroll records

- Ownership documentation

These records can be invaluable during audits or disputes.

Workers’ Compensation vs. Occupational Accident Insurance

A topic many businesses overlook is the difference between workers’ compensation insurance and occupational accident insurance.

While both provide financial protection after workplace injuries, they are not the same.

| Feature | Workers’ Compensation Insurance | Occupational Accident Insurance |

| Required by law | Often required | Usually optional |

| Covers medical expenses | Yes | Yes |

| Covers lost wages | Yes | Often limited |

| Protects employer from lawsuits | Generally yes | Usually no |

| Available to contractors | Limited | Commonly available |

| Regulated by state law | Yes | No |

Occupational accident insurance is often purchased by independent contractors, gig workers, and self-employed professionals who do not qualify for traditional workers’ compensation coverage.

While it can provide valuable protection, it does not offer the same legal protections and statutory benefits as workers’ compensation insurance.

Workers’ Compensation Exemptions in the Gig Economy

The rise of freelance and app-based work has created new questions about workers’ compensation requirements.

Workers for platforms such as ride-sharing, delivery, and freelance marketplaces are often classified as independent contractors rather than employees.

As a result, many are not automatically covered under traditional workers’ compensation systems.

Common Gig Workers Who May Be Exempt

Examples include:

- Rideshare drivers

- Food delivery drivers

- Freelancers

- Consultants

- Independent service providers

Why Classification Matters?

The legal debate surrounding gig worker classification continues across many states.

If a worker is classified as an employee, workers’ compensation coverage may become mandatory. If classified as an independent contractor, exemption rules may apply.

Because these classifications are frequently challenged in court and through legislation, businesses operating in the gig economy should pay close attention to changing regulations.

Alternative Coverage Options

Many exempt gig workers choose to purchase:

- Occupational accident insurance

- Disability insurance

- Health insurance

- Business liability coverage

These policies can help reduce financial risks when traditional workers’ compensation benefits are unavailable.

How Insurance Companies Verify Workers’ Compensation Exemptions During Audits

Many business owners assume exemption claims go unverified. In reality, insurance carriers regularly audit businesses to confirm that workers have been properly classified and covered.

What Auditors Typically Review

Insurance audits often examine:

- Payroll records

- Tax documents

- Contractor agreements

- Exemption certificates

- Ownership records

- Subcontractor documentation

The purpose is to ensure businesses are paying accurate premiums and complying with workers’ compensation laws.

Common Audit Red Flags

Auditors may investigate situations where:

- Contractors perform the same duties as employees

- Missing exemption certificates exist

- Payroll records appear incomplete

- Worker classifications frequently change

- Subcontractors lack proof of coverage

Businesses that maintain organized records are generally better positioned to pass audits without complications.

Workers’ Compensation Exemptions for Family Businesses and Startups

Family-owned businesses and startups often have unique workers’ compensation considerations.

Family Members Working in the Business

Some states provide exemptions for:

- Spouses

- Parents

- Children

- Immediate family members

However, these exemptions are not universal and vary by jurisdiction.

Startup Businesses

Many startup founders assume they are exempt because the company is new or has limited revenue.

In reality, workers’ compensation requirements are typically based on employee status rather than company age or profitability.

Once employees are hired, coverage obligations may begin immediately, depending on state law.

Why Startups Should Consider Coverage Early

Even when exemptions exist, workers’ compensation coverage can:

- Protect founders from unexpected medical expenses

- Improve credibility with investors and clients

- Support contract qualification requirements

- Reduce financial risks during business growth

The Bottom Line

Workers’ compensation exemptions can provide flexibility for certain business owners, independent contractors, and self-employed professionals. However, exemptions are not automatic and often depend on state laws, worker classifications, business structure, and industry requirements.

While independent contractors, sole proprietors, corporate officers, LLC members, volunteers, and certain agricultural or domestic workers may qualify for exemptions, incorrectly assuming exemption status can lead to significant penalties, lawsuits, and financial liability.

The safest approach is to verify your state’s requirements, maintain proper documentation, and regularly review your worker classifications. Even when coverage is not legally required, many exempt individuals choose to carry workers’ compensation insurance to protect their income, business operations, and long-term financial security.